How To Choose a Merchant Service Provider: A 10 Step Guide

To choose the right merchant services provider for your business, assess your processing needs including transaction volumes and payment channels, evaluate pricing models for total cost transparency, and verify settlement speed and security standards.

Additional considerations for businesses should be to validate system compatibility with existing software, review reporting capabilities and customer support quality, test provider systems through demos or trials, and negotiate contract terms that balance cost with flexibility.

For a detailed guide on how to choose a merchant service provider follow the 10 steps below:

1. Assess Your Processing Needs

2. Identify Required Payment Methods and Channels

3. Evaluate Pricing Models and Cost Structure

4. Assess Settlement Speed and Cash Flow

5. Verify Security and Compliance Standards

6. Validate System Compatibility and Integration

7. Evaluate Reporting and Analytics Tools

8. Assess Customer Support Quality

9. Test Provider Systems and Capabilities

10. Negotiate Contract Terms and Pricing

1. Assess Your Processing Needs

Assess your processing needs by reviewing monthly transaction volumes, average ticket size, industry-specific needs and growth expectations to determine the best provider with the right processing capacity. By assessing current monthly transaction volumes businesses can determine the more cost efficient pricing structure. Flat-rate pricing becomes more costly for businesses processing large volumes, while interchange-plus pricing scales more efficiently as transaction volume grows. For larger enterprise companies transacting over £5m a month consider choosing a merchant service provider capable of transacting high monthly volumes.

Choosing a provider with expertise in your industry can provide compliance knowledge, specialised support and industry-specific features such as tipping functionality for restaurant merchants. High-risk industries including travel, nutraceuticals, and subscription services experience high chargeback rates and require providers that understand these patterns as normal business operations.

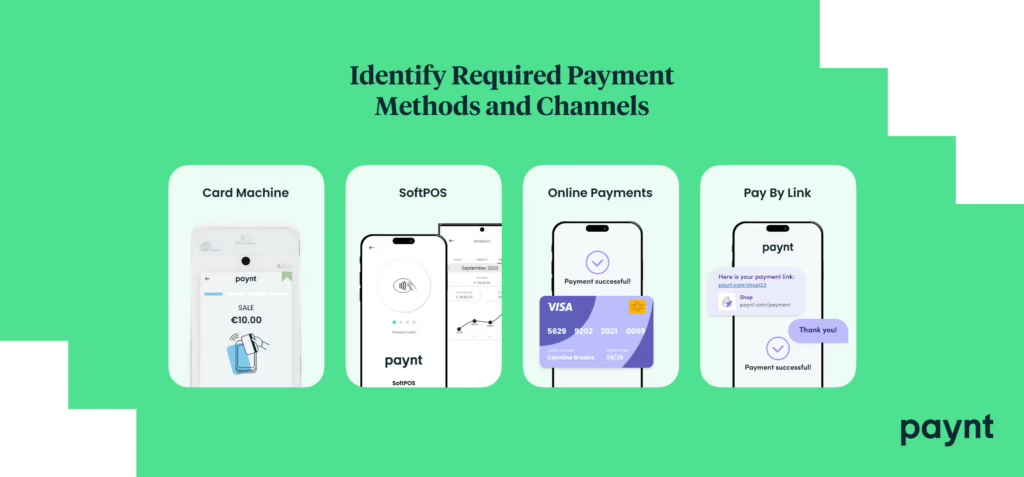

2. Identify Required Payment Methods and Channels

Identify the required payment methods and channels for your business such as credit cards, debit cards, digital wallets, invoicing, recurring billing, and transactions in-store and online. Understand the payment methods your business needs and whether the merchant service provider can provide and integrate the payment methods for your business.

List the payment methods customers currently use or will require to ensure the potential provider can match customer preferences. Digital wallets like Apple Pay, Google Pay, and Samsung Pay require NFC-enabled terminals enabling contactless transactions. E-commerce businesses need payment gateways supporting tokenisation for stored credentials that protect customer card data during repeat purchases. Subscription businesses require automated recurring billing to improve payment collection rates. For each payment method the provider should be able to accept all major credit card networks Visa, Mastercard, and American Express.

3. Evaluate Pricing Models and Cost Structure

Evaluate pricing models and cost structure of each provider based on the total effective cost for transactions, chargebacks and monthly fees for POS terminals. Merchant service providers have different pricing models such as interchange-plus, flat-rate, or tiered structures. Transaction fees, monthly fees, gateway fees, chargeback fees, equipment costs, leasing arrangements, should be calculated to estimate costs.

Interchange-plus pricing separates interchange fees set by card networks from a processor markup to provide transparent cost visibility that enables merchants to verify they are paying fair rates. Flat-rate pricing charges one percentage regardless of card type, which simplifies accounting but potentially increases costs for businesses processing mostly debit cards that have lower interchange rates.

4. Assess Settlement Speed

Assess the settlement speed of the provider by comparing settlement timeframes such as next-business-day settlement or standard 2 to 3 business days. Settlement speed determines how quickly processed payments reach business bank accounts. For providers that offer next-business-day settlements check funds are deposited within 24 hours for transactions processed before cutoff times.

5. Verify Security and Compliance Standards

Verify the security and compliance standards of the provider to protect sensitive consumer and business data. Confirm the provider maintains PCI DSS compliance, implements tokenisation and end-to-end encryption technology. PCI DSS compliance protects cardholder data through access controls, encryption standards, and monitoring procedures that reduce data breach risk.

Tokenisation replaces card numbers with random tokens which prevents stored credential breaches from exposing actual payment card data. End-to-end encryption protects data from card swipe through authorisation by ensuring payment information remains encrypted throughout the transaction process.

Fraud monitoring, chargeback alerts, and dispute tools are additional security features providers provide to protect cardholder data throughout the transaction process.

6. Check System Compatibility and Integration

Check the system compatibility and integration capabilities of the provider to current business systems and software used. Examine point-of-sale systems, card readers, existing e-commerce platforms, and integration with accounting software, inventory systems, and CRM platforms, to maintain the operational efficiency of your business.

Identify current software systems within your business that require payment integration to ensure the new provider supports existing technology infrastructure. Providers that provide API availability enables custom integrations between payment systems and business software developed specifically for unique operational requirements.

7. Evaluate Reporting and Analytics Tools

Evaluate reporting and analytics tools which provide insights into sales performance, chargeback, refunds, settlements and transaction fee costs. Analytics tools identify trends including average ticket changes, peak transaction times, card type distributions, and decline rate patterns that inform pricing strategies and staffing decisions.

Chargeback reports are helpful in tracking dispute reasons, response deadlines, and win rates to help merchants identify patterns requiring operational changes. Batch reporting summarises daily processing activity with gross sales, refunds, chargebacks, and net deposits that provide high-level financial overview for daily business operations.

8. Assess Customer Support Quality

Assess the customer support quality of the provider by business hours availability, accessible channels like telephone, email, and live chat, and dedicated account management. Providers with twenty-four hour support systems help prevent extended downtime where payment systems fail temporarily. For businesses operating during the weekend technical support outside of normal business days are crucial.

Telephone support enables immediate troubleshooting. Troubleshooting by a provider addresses urgent terminal failures or authorisation problems. Live chat provides quick answers for routine questions and eliminates telephone hold times. Dedicated account managers are assigned to specific merchants to provide personalised service and faster escalation paths compared to standard customer support.

9. Test Provider Systems and Capabilities

Test provider systems and capabilities by requesting demos or trial periods to evaluate actual transaction processing, settlement timing, integration compatibility, and support responsiveness. Live demonstrations reveal actual system interfaces, transaction workflows, and reporting capabilities. Request access to test environments to enable hands-on testing of payment gateway interfaces without financial risk.

Sandbox environments help businesses test integrations between payment gateways and existing business software without processing live transactions. Process sample transactions across different card types including credit cards, debit cards, and digital wallets to verify authorisation speed and success rates.

10. Negotiate Contract Terms and Pricing

Negotiate contract terms and pricing by comparing written proposals, review contract lengths, termination fees and confirming implementation timelines. Request written proposals which itemise all fees including transaction rates for different card types, monthly minimums, gateway fees, PCI compliance fees, chargeback fees and equipment costs. Request the providers policies on changing fee structure when business transaction volumes increase and equipment upgrades to facilitate future growth.

What Merchant Services Does Paynt Offer?

Paynt provides businesses with the infrastructure to accept credit cards, debit cards, and digital wallet payments across physical and online channels. At Merchant Service Provider Paynt specialise in serving restaurants, retail stores, and service businesses requiring integrated payment solutions with next-day settlement capabilities. Below are the merchant services which Paynt offers:

- POS terminal options: Access to countertop terminals, handheld tableside devices, and mobile card readers suited to different business environments and service styles.

- Online and remote payment capabilities: Accept payments online through integrated website payment gateways, Pay by Link for email and SMS invoicing, virtual terminals for telephone orders, and recurring billing for subscription-based services.

- Tip management and compliance: Tip functionality on payment terminals with compliant and automated tip pooling systems for staff compensation management.

- Next-day settlement and merchant funding: Payment processing with next-day settlement that ensures optimal cash flow management, plus access to merchant cash advances for working capital needs.

- Customer support: Dedicated account management and technical assistance during business hours with escalation paths for urgent issues.

- Security and PCI compliance: Cardholder data protection through encryption, tokenisation, and PCI DSS compliance that meets card network security requirements.

- Fraud prevention and chargeback management: Transaction monitoring for suspicious activity, high-risk payment flagging, dispute tracking tools, and evidence submission for representment.